From Chaos to Clarity: A Response to FCA DP25/1 on Cryptoasset Regulation

Why the FCA’s crypto paper gets it half right, and what it still doesn’t understand about next-gen investing.

1. Executive Summary

The FCA’s Discussion Paper 25/1 is a vital step towards regulating digital assets, but its focus remains rooted in legacy finance. As the founder of The Engagement Appeal (TEA), with 20+ years in shareholder engagement, I’ve seen how inclusive systems drive market vitality. In 2024, I immersed myself in crypto as a retail investor to understand the next generation. They’re not reckless—they’re demanding access, clarity, and agency. Regulation must empower, not alienate, these 23 million UK retail investors who hold £261 billion in shares. This response urges the FCA to prioritise literacy, inclusion, and asset differentiation to build a future-ready financial system.

2. Context: Why This Matters Now

The FCA aims to protect consumers and ensure market stability, but crypto reflects deeper shifts: distrust in traditional finance, technological acceleration, and a desire for financial autonomy. TEA’s 2024 research shows 60% of Gen Z have invested, making them the most active retail cohort. They seek relevance, not regulation avoidance. Ignoring this risks driving activity offshore or underground. Regulators must engage these investors as partners, not just subjects.

3. Bitcoin vs. the Crypto Complex

The FCA’s paper treats all cryptoassets as one, missing a critical distinction:

Bitcoin: A decentralised monetary network, akin to digital property, with no issuer or speculative yield.

Other Cryptoassets: Altcoins, tokens, and DeFi platforms, often tied to issuers and higher risk.

Regulating Bitcoin like speculative tokens is like treating gold and NFTs identically—it distorts policy and stifles innovation.

4. Engagement as Risk Mitigation

Crypto’s volatility stems partly from poor literacy and inaccessible platforms. Retail investors learn via trial, error, or social media, not structured education. TEA’s work shows that engaged, informed investors drive transparency and accountability. Regulation must prioritise clear communication and inclusive dialogue to reduce risk and empower users.

5. Applauding the Right Moves

The FCA’s proposals are commendable:

Scrutinising cryptoasset trading platforms (CATPs) that mix roles like market-making and custody.

Restricting high-risk staking and lending products.

Considering limits on credit-based crypto purchases.

These protect consumers but need complementary measures to ensure access and education.

6. Where the Paper Falls Short

Undifferentiated Approach: Failing to segment Bitcoin from other cryptoassets risks overregulation of stable systems and underregulation of speculative ones.

Top-Down Bias: Proposals prioritise institutional needs, sidelining retail voices.

Missed Opportunity: Overemphasising risk ignores crypto’s potential to democratise finance and engage new investors.

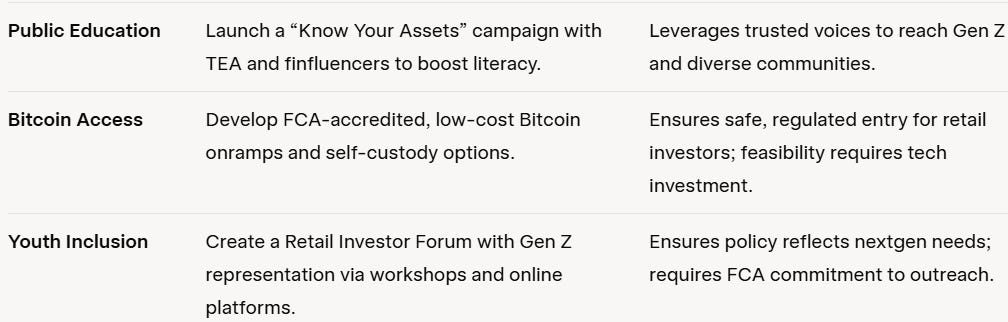

7. Recommendations

8. Final Thoughts: From Watchdog to Partner

The FCA can lead globally by building an inclusive, adaptive regulatory framework. Consumer protection must mean consumer empowerment—through literacy, access, and dialogue. The future of finance is digital, fractional, and decentralised. The UK must design for this reality, not defend the past, to harness the potential of its retail investors.

📩 Contact

Sheryl Cuisia

Founder & CEO, The Engagement Appeal

📬 sheryl@teaxall.org

🔗 sherylinmotion.substack.com

📱 @sherylinmotion

⸻

References

FCA DP25/1: Regulating Cryptoasset Activities (2025).

TEA White Paper (2024): teaxall.org/white-paper.

TEA Human Impact Index (2024): teaxall.org/finglitz-human-impact-index.

FCA page: https://www.fca.org.uk/publications/discussion-papers/dp25-1-regulating-cryptoasset-activities

Paper: https://www.fca.org.uk/publication/discussion/dp25-1.pdf